http://altlantic-internationalpartnership.com/2011/05/atlantic-international-partnership-headlines-who-are-gaddafi%E2%80%99s-on-screen-supporters/

Of course Reuters has reporters on both sides of the front line, but from Tunis I have been keeping an eye on Libyan television too – partly because it has scrolling headlines in English about the latest crusader, colonial and al Qaeda atrocities which might carry some news but also, I have to admit, from a fascination with the procession of people voicing their support for the Brother Leader, Muammar Gaddafi.

Not being an Arabic speaker, I can only gather a few words, but the raised voices make clear the emotion, often from Gaddafi’s Bab al Aziziyah compound itself.

Who are these Libyans and what do they really feel? Who are the people who bring young children on their shoulders to this repeatedly bombed compound, dressing them in bright green patriotic suits like little elves and hoisting them high while they thrust fists in the air?

Through the day the voices change – at one point a talk show host with improbably red hair discusses with participants sat in armchairs in the sunshine of the Mediterranean spring.

A succession of people take the microphone to voice their opinion – pretty much the same opinion. Sometimes they are teenagers, sometimes workers, sometimes in uniform, sometimes old men in sunglasses – always speaking quickly, loudly and angrily.

Do people get paid for their appearances or is it worth it for the few minutes of fame? Do they volunteer? Are they forced to do this?

Then the crowds build, waving pictures of Gaddafi from various eras – the young colonel in the years after he seized power more than four decades ago, the guide in the dress of a desert nomad, the leader in ‘King of Pop’-style uniforms covered in braid. Fists are thrust skyward again.

Sometimes there are gunshots of celebration in the air. Once, some spectators appeared on horseback. Another day, a group seemed to burst spontaneously into the streets around the compound, sweeping their green flags in joy as though taking an early day off from school.

At night the lights might come out for a pop concert, the crowd swaying to the rhythm and patriotic lyrics.

Is attendance obligatory or is it the best entertainment on offer in Tripoli? Once you are there, do you get overtaken by the mood of solidarity and patriotism? When you go home to do you feel energised? Do you feel relieved to have escaped unscathed? Uneasy at your part in what even the most charitable would have to call propaganda? Is it all just in a day’s work?

Even being in Tripoli wouldn’t necessarily help to answer these questions. As my colleague Lin Noueihed wrote from there, the fear is palpable and getting an honest opinion from anyone is almost impossible.

It would seem insulting to brand all the people appearing on television as mere sycophants. Tripoli has been bombed repeatedly. The very compound has been targeted – according to Libyan officials killing several members of Gaddafi’s family plus security guards and office workers. There is reason to be angry, but also plenty of reason to be afraid.

Unfortunately, while we don’t know those people have the freedom to say what they believe, we also have to question whether we can believe anything they say. One day, I hope to find out.

Thursday, May 12, 2011

Atlantic International Partnership Headlines: Stock Market News for May 4, 2011

http://altlantic-internationalpartnership.com/2011/05/atlantic-international-partnership-headlines-stock-market-news-for-may-4-2011/

On Tuesday, markets felt the pinch of disappointing quarterly results and the benchmarks slid a few points as investors feared profitability might drop over the coming quarters. Over the past couple of weeks, markets have remained upbeat, climbing to multi-year highs following robust corporate results. Additionally, a drop in crude prices weighed down the energy sector.

The Dow Jones Industrial Average (DJIA) was the only gainer among the benchmarks as it edged up 0.2% to 12,807.51. The Standard & poor 500 dropped 0.3% and the Nasdaq slipped 0.8% to settle at 1,356.62 and 12,807.51, respectively. After hitting its highest level in three years last week, the S&P 500 has now declined for two-straight days. On the New York Stock Exchange, composite volumes were at 4.5 billion shares. For every one stock that advanced on the NYSE, two stocks declined.

While earnings had been a favorable factor for the markets over the past few weeks, the markets had to suffer the flip side as companies posted lower-than-expected results yesterday. Pfizer Inc. (NYSE:PFE – Analyst Report) (2.8%) was one of the biggest laggards for the Dow as it failed to beat sales estimates. Joining the list of disappointing results were companies like Clorox Corporation (NYSE:CLX – Analyst Report), Molson Coors Brewing Company (NYSE:TAP – Analyst Report), Beazer Homes USA Inc. (NYSE:BZH – Snapshot Report) and Sears Holdings Corporation (NASDAQ:SHLD – Analyst Report). These shares dropped 3.6%, 6.0%, 5.0% and 9.9%, respectively.

Pfizer Inc. posted a heavily disappointing result. Earnings for the quarter managed to top estimates but shares slid significantly as the drug major failed to cross revenue estimates. Moreover, the company also lowered its revenue guidance. Pfizer Inc. reported first quarter earnings of 60 cents per share, flat from the year-ago period. First quarter revenues declined 0.4% to $16.5 billion. Shares were down 2.8% and finally closed at $20.44.

Meanwhile, Cognizant Technology Solutions Corp. (NASDAQ:CTSH – Analyst Report) reported revenues of $1.37 billion in the first quarter of 2011, up 42.9% year over year and up 4.6% sequentially. Net income came in at $208.3 million or 67 cents per diluted share compared to a net income of $151.5 million or 49 cents per share in the year-ago quarter. Cognizant Technology’s figures managed to beat estimates but its slowing growth rate dragged the shares down. The company’s shares dropped 5.75 to settle at $77.52.

As crude prices retreated, energy shares slid into the red, dragging down the broader markets. The June crude oil contract dropped $2.47 and settled at $111.05 a barrel Exxon Mobil Corporation (NYSE:XOM – Analyst Report), ConocoPhillips (NYSE:COP – Analyst Report), Chevron Corp. (NYSE:CVX – Analyst Report), Valero Energy Corp. (NYSE:VLO – Analyst Report) and Western Refining Inc. (NYSE:WNR – Analyst Report) dropped 1.6%, 3.8%, 1.9%, 2.8% and 3.4%, respectively.

Economic data, released on Tuesday did little to boost market sentiment. The Commerce Department reported that Factory Orders increased by 3.0%, $13.5 billion, to $462.9 billion in March against expectations that the measure would increase by 1.9%, following a 0.7% increase in February. Factory Orders are up following five consecutive monthly increases. Excluding transportation, Factory Orders increased by 2.6%.

On Tuesday, markets felt the pinch of disappointing quarterly results and the benchmarks slid a few points as investors feared profitability might drop over the coming quarters. Over the past couple of weeks, markets have remained upbeat, climbing to multi-year highs following robust corporate results. Additionally, a drop in crude prices weighed down the energy sector.

The Dow Jones Industrial Average (DJIA) was the only gainer among the benchmarks as it edged up 0.2% to 12,807.51. The Standard & poor 500 dropped 0.3% and the Nasdaq slipped 0.8% to settle at 1,356.62 and 12,807.51, respectively. After hitting its highest level in three years last week, the S&P 500 has now declined for two-straight days. On the New York Stock Exchange, composite volumes were at 4.5 billion shares. For every one stock that advanced on the NYSE, two stocks declined.

While earnings had been a favorable factor for the markets over the past few weeks, the markets had to suffer the flip side as companies posted lower-than-expected results yesterday. Pfizer Inc. (NYSE:PFE – Analyst Report) (2.8%) was one of the biggest laggards for the Dow as it failed to beat sales estimates. Joining the list of disappointing results were companies like Clorox Corporation (NYSE:CLX – Analyst Report), Molson Coors Brewing Company (NYSE:TAP – Analyst Report), Beazer Homes USA Inc. (NYSE:BZH – Snapshot Report) and Sears Holdings Corporation (NASDAQ:SHLD – Analyst Report). These shares dropped 3.6%, 6.0%, 5.0% and 9.9%, respectively.

Pfizer Inc. posted a heavily disappointing result. Earnings for the quarter managed to top estimates but shares slid significantly as the drug major failed to cross revenue estimates. Moreover, the company also lowered its revenue guidance. Pfizer Inc. reported first quarter earnings of 60 cents per share, flat from the year-ago period. First quarter revenues declined 0.4% to $16.5 billion. Shares were down 2.8% and finally closed at $20.44.

Meanwhile, Cognizant Technology Solutions Corp. (NASDAQ:CTSH – Analyst Report) reported revenues of $1.37 billion in the first quarter of 2011, up 42.9% year over year and up 4.6% sequentially. Net income came in at $208.3 million or 67 cents per diluted share compared to a net income of $151.5 million or 49 cents per share in the year-ago quarter. Cognizant Technology’s figures managed to beat estimates but its slowing growth rate dragged the shares down. The company’s shares dropped 5.75 to settle at $77.52.

As crude prices retreated, energy shares slid into the red, dragging down the broader markets. The June crude oil contract dropped $2.47 and settled at $111.05 a barrel Exxon Mobil Corporation (NYSE:XOM – Analyst Report), ConocoPhillips (NYSE:COP – Analyst Report), Chevron Corp. (NYSE:CVX – Analyst Report), Valero Energy Corp. (NYSE:VLO – Analyst Report) and Western Refining Inc. (NYSE:WNR – Analyst Report) dropped 1.6%, 3.8%, 1.9%, 2.8% and 3.4%, respectively.

Economic data, released on Tuesday did little to boost market sentiment. The Commerce Department reported that Factory Orders increased by 3.0%, $13.5 billion, to $462.9 billion in March against expectations that the measure would increase by 1.9%, following a 0.7% increase in February. Factory Orders are up following five consecutive monthly increases. Excluding transportation, Factory Orders increased by 2.6%.

Atlantic International Partnership Headlines:Facebook: Now Serving Over 500 Million Users and 346 Billion Ads

http://altlantic-internationalpartnership.com/2011/05/facebook-now-serving-over-500-million-users-and-346-billion-ads/

On his Facebook page, Mark Zuckerberg explains that his social networking site is fashioning a more open world where people can “share what’s important to them.” Increasingly, the world’s advertisers are also leveraging the platform to share what’s important to them–to the tune of 346 billion display ad impressions in the first quarter of 2011.

ComScore is reporting today that Facebook doubled the number of ads it delivered during the same period last year and crushed all other online publishers, serving a whopping one in three online ads in the U.S. Yahoo, Microsoft, AOL, and Google rounded out the top five (AOL’s display advertising, in fact, has been a bright spot in the company’s otherwise dismal financial performance). The ranks of the top online advertisers were dominated by finance and telecom: AT&T finished first, followed by the credit information company Experian, the online trading and investing company Scottrade, the accounting software company Intuit, and Verizon (we were surprised the acai berry people didn’t make the cut). In all, America’s internet users were flooded with over one trillion ads during the quarter.

Erick Schonfeld at TechCrunch explains that Facebook’s strong performance doesn’t necessarily mean the company is stealthily transforming social networking into a blaring billboard. Facebook’s growing popularity allows it serve more ads on more pages, Schonfeld notes, and the company is also experimenting with social ads that look more like News items shared by friends.

ComScore is reporting today that Facebook doubled the number of ads it delivered during the same period last year and crushed all other online publishers, serving a whopping one in three online ads in the U.S. Yahoo, Microsoft, AOL, and Google rounded out the top five (AOL’s display advertising, in fact, has been a bright spot in the company’s otherwise dismal financial performance). The ranks of the top online advertisers were dominated by finance and telecom: AT&T finished first, followed by the credit information company Experian, the online trading and investing company Scottrade, the accounting software company Intuit, and Verizon (we were surprised the acai berry people didn’t make the cut). In all, America’s internet users were flooded with over one trillion ads during the quarter.

Erick Schonfeld at TechCrunch explains that Facebook’s strong performance doesn’t necessarily mean the company is stealthily transforming social networking into a blaring billboard. Facebook’s growing popularity allows it serve more ads on more pages, Schonfeld notes, and the company is also experimenting with social ads that look more like News items shared by friends.

Atlantic International Partnership Headlines: Berkshire stands by investment in BYD

http://altlantic-internationalpartnership.com/2011/05/atlantic-international-partnership-headlines-berkshire-stands-by-investment-in-byd/

(Reuters) – Berkshire Hathaway is happy with its investment in Chinese car maker BYD Co Ltd, despite product delays and declining sales, Berkshire’s vice chairman Charlie Munger said on Saturday.

Munger and Warren Buffett were asked at the company’s annual meeting whether they still considered BYD a good investment despite the company’s recent problems.

“I’m quite encouraged by what’s going on, and I expect delays and glitches,” said Munger. Buffett has said that Munger was the inspiration for Berkshire’s September 2008 purchase of nearly 10 percent of BYD.

BYD’s March sales were down more than 40 percent from a year earlier, and its entry into the U.S. market has been repeatedly delayed. Munger said such growing pains were natural given BYD’s aggressive growth plans

(Reuters) – Berkshire Hathaway is happy with its investment in Chinese car maker BYD Co Ltd, despite product delays and declining sales, Berkshire’s vice chairman Charlie Munger said on Saturday.

Munger and Warren Buffett were asked at the company’s annual meeting whether they still considered BYD a good investment despite the company’s recent problems.

“I’m quite encouraged by what’s going on, and I expect delays and glitches,” said Munger. Buffett has said that Munger was the inspiration for Berkshire’s September 2008 purchase of nearly 10 percent of BYD.

BYD’s March sales were down more than 40 percent from a year earlier, and its entry into the U.S. market has been repeatedly delayed. Munger said such growing pains were natural given BYD’s aggressive growth plans

Wednesday, May 11, 2011

Atlantic International Partnership Headlines: Teaching new dogs old tricks

http://altlantic-internationalpartnership.com/2011/04/atlantic-international-partnership-headlines-teaching-new-dogs-old-tricks/

Remember that scene in “Mr. Smith Goes to Washington” when Jimmy Stewart arrives in the capital for the first time? The freshman senator shakes off his handlers in Union Station and jumps onto a sightseeing bus, eager to see all the statues and monuments honoring the greats of American history.

“I don’t think I’ve ever been so thrilled in my life,” he says afterward. “And that Lincoln Memorial — gee whiz! Mr. Lincoln, there he is. Just looking straight at you as you come up those steps. Just sitting there like he was waiting for somebody to come along.”

For all their talk of the Founding Fathers, the Constitution and core principles, you’d have thought that the current freshman class of Congress, the sprouted seed of Tea Partyers and the 2010 midterms, would have made a similar tour their first priority on arrival. And for all I know, many of them did just that. But for some, the siren song of cash and influence has proven stronger, already luring them onto the rocks of privilege and corruption that lurk just inside the Beltway. They’ve made a beeline not for the hallowed shrines of patriots’ pride but for the elegant suites of K Street lobbyists, where the closest its residents have been to Lincoln is the bearded face peering from the $5 bill — chump change. So much for fiercely resisting the wicked, wicked ways of Washington. These new members were seduced faster than Dustin Hoffman in “The Graduate.”

In an April 2 editorial, the New York Times reported:

AP/Susan Walsh

House Speaker John Boehner of Ohio delivers the oath of office to Republican members of the House of Representatives during the first session of the 112th Congress, on Capitol Hill in Washington, Wednesday, Jan. 5, 2011.

“I don’t think I’ve ever been so thrilled in my life,” he says afterward. “And that Lincoln Memorial — gee whiz! Mr. Lincoln, there he is. Just looking straight at you as you come up those steps. Just sitting there like he was waiting for somebody to come along.”

For all their talk of the Founding Fathers, the Constitution and core principles, you’d have thought that the current freshman class of Congress, the sprouted seed of Tea Partyers and the 2010 midterms, would have made a similar tour their first priority on arrival. And for all I know, many of them did just that. But for some, the siren song of cash and influence has proven stronger, already luring them onto the rocks of privilege and corruption that lurk just inside the Beltway. They’ve made a beeline not for the hallowed shrines of patriots’ pride but for the elegant suites of K Street lobbyists, where the closest its residents have been to Lincoln is the bearded face peering from the $5 bill — chump change. So much for fiercely resisting the wicked, wicked ways of Washington. These new members were seduced faster than Dustin Hoffman in “The Graduate.”

In an April 2 editorial, the New York Times reported:

Since last year’s Republican victories, nearly 100 lawmakers have hired former lobbyists as their chiefs of staff or legislative directors, according to data compiled by two watchdog groups, the Center for Responsive Politics and Remapping Debate. That is more than twice as many as in the previous two years.

In that same period, 40 lobbyists have been hired as staff members of Congressional committees and subcommittees, the boiler rooms where legislation is drafted. That again dwarfs the number from the previous two years. While some of those lobbyist-staffers were hired by Democrats, the vast majority are working for Republicans… In many cases, those hiring lobbyists were Tea Party candidates who vowed to end business as usual in Washington.

The revolving door between government and lobbyists has never spun faster. Then there’s this, from Wednesday”s Washington Post:

According to the nonpartisan Sunlight Foundation, Rep. Noem, who pledged to voters not to make Washington her home, held at least 10 fundraisers in D.C. during that first quarter, her first months as a member of Congress. They included two dinners at the Capital Grille, at which attendees donated between $1,500 and $2,000 apiece, and lunch at We, the Pizza on Pennsylvania Avenue.

A CQ MoneyLine study reports that during the first three months of the year the 87 Republican freshmen pulled in a total of $14.7 million from individuals as well as PACs. Leading the crowd was Diane Black of Tennessee with $926,000, but more than two-thirds of it was her own money. In second place was West Virginia’s David B. McKinley, with $540,000.

Rep. McKinley was one of nine new GOP members spotlighted this week by the website Politico as members who have done things “the Washington way, using a legislative process they once railed against to try to assist donors, protect favored industries or settle scores with their political enemies.”

Three weeks after his swearing in, McKinley introduced a bill to overturn an Environmental Protection Agency ruling that vetoed an Army Corps of Engineers water permit for mountaintop mining, the practice that blasts the tops off mountains and sends debris raining down on communities, streams and rivers. The bill has ramifications for the entire mining industry, but the specific mine in question is owned by Arch Coal. Its PAC contributed $2,500 to McKinley’s 2010 election campaign and another thousand so far this year.

The mining industry was McKinley’s largest corporate campaign contributor — $51,751. And a month after he took office, Politico reported, he introduced another bill “that would block a proposed EPA regulation against coal-ash bricks and drywall, materials architectural and engineering firms — such as one founded by McKinley — routinely recommend in construction project bids.”

Others cited by the Politico investigation include freshmen Bill Johnson of Ohio and Morgan Griffith of Virginia. They, too, have been going to bat for mine executives. The mining sector was Johnson’s biggest corporate donor at $25,146; same with Griffith, who received $40,450.

Texas freshman Bill Flores has been going after the Interior Department’s procedures for offshore oil drilling permits, trying to get the department to impose tighter deadlines and pay back billions in leasing rights to oil companies whose permits are denied. He’s the former president and CEO of an exploratory oil firm. Its employees were his second largest campaign contributor and the oil and gas industry threw in more than $200,000.

In rebuttal, the office of each congressman has generated the appropriate, high-minded spin. “West Virginia is coal, and coal is West Virginia,” said McKinley’s spokeswoman. “He’s doing what he said he would — fighting tooth and nail to stop the EPA’s war on coal …” Rep. Flores told Politico, “This is an issue that is very important to me as I have been involved in finding solutions to America’s long-term energy independence for the last thirty years.”

And so it goes. At this rate, if the Abraham Lincoln so venerated by the idealistic Mr. Smith is still at his memorial hoping for someone to come along, someone with integrity and dedication to the people and not the almighty dollar, he’s going to have a long wait.

The new dogs have learned the old tricks of Capitol Hill with remarkable speed, and their big business masters, armed with their Supreme Court-sanctioned ability to throw bottomless bags of money around, have more control of the leash than ever.

Michael Winship, senior writing fellow at Demos and president of the Writers Guild of America, East, is former senior writer of “Bill Moyers Journal” on PBS.

Many of the Republican freshmen in the House won election vowing to shake up Washington, so it’s a little surprising that many of them seem to be playing an old Washington game: raising much of their campaign money from corporate political action committees.For example, freshman star Kristi Noem of South Dakota — one of the two newbies anointed as liaison to the Republican House leadership — raised $169,000 in PAC money, including cash from General Electric, Boeing, Raytheon, Wells Fargo, Fedex, AFLAC, Altria (the parent company of Philip Morris and Kraft Foods) and pharmaceutical giants Bayer and GlaxoSmithKline.

More than 50 members of the class of 87 GOP freshmen took in more than $50,000 from PACs during the first quarter of 2011, according to new campaign disclosure reports filed with the Federal Election Commission. Eighteen of the lawmakers took in more than $100,000.

According to the nonpartisan Sunlight Foundation, Rep. Noem, who pledged to voters not to make Washington her home, held at least 10 fundraisers in D.C. during that first quarter, her first months as a member of Congress. They included two dinners at the Capital Grille, at which attendees donated between $1,500 and $2,000 apiece, and lunch at We, the Pizza on Pennsylvania Avenue.

A CQ MoneyLine study reports that during the first three months of the year the 87 Republican freshmen pulled in a total of $14.7 million from individuals as well as PACs. Leading the crowd was Diane Black of Tennessee with $926,000, but more than two-thirds of it was her own money. In second place was West Virginia’s David B. McKinley, with $540,000.

Rep. McKinley was one of nine new GOP members spotlighted this week by the website Politico as members who have done things “the Washington way, using a legislative process they once railed against to try to assist donors, protect favored industries or settle scores with their political enemies.”

Three weeks after his swearing in, McKinley introduced a bill to overturn an Environmental Protection Agency ruling that vetoed an Army Corps of Engineers water permit for mountaintop mining, the practice that blasts the tops off mountains and sends debris raining down on communities, streams and rivers. The bill has ramifications for the entire mining industry, but the specific mine in question is owned by Arch Coal. Its PAC contributed $2,500 to McKinley’s 2010 election campaign and another thousand so far this year.

The mining industry was McKinley’s largest corporate campaign contributor — $51,751. And a month after he took office, Politico reported, he introduced another bill “that would block a proposed EPA regulation against coal-ash bricks and drywall, materials architectural and engineering firms — such as one founded by McKinley — routinely recommend in construction project bids.”

Others cited by the Politico investigation include freshmen Bill Johnson of Ohio and Morgan Griffith of Virginia. They, too, have been going to bat for mine executives. The mining sector was Johnson’s biggest corporate donor at $25,146; same with Griffith, who received $40,450.

Texas freshman Bill Flores has been going after the Interior Department’s procedures for offshore oil drilling permits, trying to get the department to impose tighter deadlines and pay back billions in leasing rights to oil companies whose permits are denied. He’s the former president and CEO of an exploratory oil firm. Its employees were his second largest campaign contributor and the oil and gas industry threw in more than $200,000.

In rebuttal, the office of each congressman has generated the appropriate, high-minded spin. “West Virginia is coal, and coal is West Virginia,” said McKinley’s spokeswoman. “He’s doing what he said he would — fighting tooth and nail to stop the EPA’s war on coal …” Rep. Flores told Politico, “This is an issue that is very important to me as I have been involved in finding solutions to America’s long-term energy independence for the last thirty years.”

And so it goes. At this rate, if the Abraham Lincoln so venerated by the idealistic Mr. Smith is still at his memorial hoping for someone to come along, someone with integrity and dedication to the people and not the almighty dollar, he’s going to have a long wait.

The new dogs have learned the old tricks of Capitol Hill with remarkable speed, and their big business masters, armed with their Supreme Court-sanctioned ability to throw bottomless bags of money around, have more control of the leash than ever.

Michael Winship, senior writing fellow at Demos and president of the Writers Guild of America, East, is former senior writer of “Bill Moyers Journal” on PBS.

Atlantic International Partnership Headlines: China as Number One? Don’t Bet Your Bottom Dollar

http://altlanticinternationalpartnership.net/2011/05/atlantic-international-partnership-headlines-china-as-number-one-don%E2%80%99t-bet-your-bottom-dollar/

Tired of Afghanistan and all those messy, oil-ish wars in the Greater Middle East that just don’t seem to pan out? Count on one thing: part of the U.S. military feels just the way you do, especially a largely sidelined Navy — and that’s undoubtedly one of the reasons why, a few months back, the specter of China as this country’s future enemy once again reared its ugly head.

Back before 9/11, China was, of course, the favored future uber-enemy of Secretary of Defense Donald Rumsfeld and all those neocons who signed onto the Project for the New American Century and later staffed George W. Bush’s administration. After all, if you wanted to build a military beyond compare to enforce a long-term Pax Americana on the planet, you needed a nightmare enemy large enough to justify all the advanced weapons systems in which you planned to invest.

As late as June 2005, neocon journalist Robert Kaplan was still writing in the Atlantic about “How We Would Fight China,” an article with this provocative subhead: “The Middle East is just a blip. The American military contest with China in the Pacific will define the twenty-first century. And China will be a more formidable adversary than Russia ever was.” As everyone knows, however, that “blip” proved far too much for the Bush administration.

Finding itself hopelessly bogged down in two ground wars with rag-tag insurgency movements on either end of the Greater Middle Eastern “mainland,” it let China-as-Monster-Enemy slip beneath the waves. In the process, the Navy and, to some extent, the Air Force became adjunct services to the Army (and the Marines). In Iraq and Afghanistan, for instance, U.S. Navy personnel far from any body of water found themselves driving trucks and staffing prisons.

It was the worst of times for the admirals, and probably not so great for the flyboys either, particularly after Secretary of Defense Robert Gates began pushing pilotless drones as the true force of the future. Naturally, a no-dogfight world in which the U.S. military eternally engages enemies without significant air forces is a problematic basis for proposing future Air Force budgets.

There’s no reason to be surprised then that, as the war in Iraq began to wind down in 2009-2010, the “Chinese naval threat” began to quietly reemerge. China was, after all, immensely economically successful and beginning to flex its muscles in local territorial waters. The alarms sounded by military types or pundits associated with them grew stronger in the early months of 2011 (as did news of weapons systems being developed to deal with future Chinese air and sea power). “Beware America, time is running out!” warned retired Air Force lieutenant general and Fox News contributor Thomas G. McInerney while describing China’s first experimental stealth jet fighter.

Others focused on China’s “string of pearls”: a potential set of military bases in the Indian Ocean that might someday (particularly if you have a vivid imagination) give that country control of the oil lanes. Meanwhile, Kaplan, whose book about rivalries in that ocean came out in 2010, was back in the saddle, warning: “Now the United States faces a new challenge and potential threat from a rising China which seeks eventually to push the U.S. military’s area of operations back to Hawaii and exercise hegemony over the world’s most rapidly growing economies.” (Head of the U.S. Pacific Command Admiral Robert Willard claimed that China had actually taken things down a notch at sea in the early months of 2011 — but only thanks to American strength.)

Atlantic International Partnership Headlines:Pakistan warns U.S.: No more raids

http://altlanticinternationalpartnership.net/2011/05/atlantic-international-partnership-headlinespakistan-warns-u-s-no-more-raids/

ISLAMABAD – Pakistan warned America Thursday of “disastrous consequences” if it carries out any more unauthorized raids against suspected terrorists like the one that killed Osama bin Laden.

However, the government in Islamabad stopped short of labeling Monday’s helicopter raid on bin Laden’s compound not far from the capital Islamabad as an illegal operation and insisted relations between Washington and Islamabad remain on course.

The army and the government have come under criticism domestically for allowing the country’s sovereignty to be violated. Some critics have expressed doubts about government claims that it was not aware of the raid until after it was over.

Special Report: The Killing of Osama bin Laden

Foreign Secretary Salman Bashir’s remarks seemed to be aimed chiefly at addressing that criticism.

“The Pakistan security forces are neither incompetent nor negligent about their sacred duty to protect Pakistan,” he told reporters. “There shall not be any doubt that any repetition of such an act will have disastrous consequences,” he said.

Bashir repeated Pakistani claims that it did not know anything about the raid until it was too late to stop it. He said the army scrambled two F-16 fighter jets when it was aware that foreign helicopters were hovering over the city of Abbottabad, but they apparently did not get to the choppers on time.

American officials have said they didn’t inform Pakistan in advance, fearing bin Laden could be tipped off.

ISLAMABAD – Pakistan warned America Thursday of “disastrous consequences” if it carries out any more unauthorized raids against suspected terrorists like the one that killed Osama bin Laden.

However, the government in Islamabad stopped short of labeling Monday’s helicopter raid on bin Laden’s compound not far from the capital Islamabad as an illegal operation and insisted relations between Washington and Islamabad remain on course.

The army and the government have come under criticism domestically for allowing the country’s sovereignty to be violated. Some critics have expressed doubts about government claims that it was not aware of the raid until after it was over.

Special Report: The Killing of Osama bin Laden

Foreign Secretary Salman Bashir’s remarks seemed to be aimed chiefly at addressing that criticism.

“The Pakistan security forces are neither incompetent nor negligent about their sacred duty to protect Pakistan,” he told reporters. “There shall not be any doubt that any repetition of such an act will have disastrous consequences,” he said.

Bashir repeated Pakistani claims that it did not know anything about the raid until it was too late to stop it. He said the army scrambled two F-16 fighter jets when it was aware that foreign helicopters were hovering over the city of Abbottabad, but they apparently did not get to the choppers on time.

American officials have said they didn’t inform Pakistan in advance, fearing bin Laden could be tipped off.

Atlantic International Partnership Headlines:Money literally could not buy this kind of publicity for Brand Britain

http://altlanticinternationalpartnership.net/2011/05/atlantic-international-partnership-headlinesmoney-literally-could-not-buy-this-kind-of-publicity-for-brand-britain/

What does the UK economy get out of the Royal wedding? That might seem a rather nerdy question to pose, just the sort of question that justifies economics’ soubriquet of “the dismal science”.

Any tally of the additional money spent by visitors, setting that off against the loss of output because of the extra bank holiday, does have a dismal ring to it. But what lifts the whole matter to a different level is the value and role of a brand. On its ability to attract a global television audience, the British Royal family would appear to be the greatest brand on earth. But is it worth anything?

On conventional arithmetic the impact of the wedding on the economy looks to be broadly neutral, maybe slightly positive. On the one hand it is disruptive, not just because of the extra day of holiday but because it comes in the middle of a whole wodge of extra days off, with the late Easter jumbling up with the early May bank holiday. You would normally expect any lost output to be recovered quickly, as common sense would suggest. But if you look back at the precedent of the Queen’s Golden Jubilee in June 2002, there was indeed a sharp fall in industrial output that was not immediately offset by subsequent gains.

On the other hand, the wedding is global in a way the jubilee was not and the commercial sector in London has responded vigorously to the occasion, with all sorts of incentives for visitors to part with their cash. There has been a boom in tourist numbers with estimates varying from 200,000 to 600,000 extra visitors. And I suppose all those foreign news crews who were developing coverage for the two billion viewers must have spent a fair amount extra too.

PricewaterhouseCoopers (PwC) has attempted to put some numbers on this whole thing, estimating that some 550,000 people will witness the event in or around Westminster; that 560,000 people will have travelled to the capital and that the commercial benefit to the London economy would be £107m. That is helpful, particularly at a time such as this, but it is not huge in the context of a regional economy of upwards of £200bn a year. It depends on how you measure it, but I saw calculations recently that ranked the London economy as the third-largest in the world, behind only New York and Tokyo. PwC notes that the Olympics next year is expected to attract more than 10 times the number of visitors, and that they will stay for around a fortnight, not just a day.

Put all this together and I would guess that there is a net plus, particularly to London, but it will not be huge in the context of the whole economy. But in the longer term it reinforces the British brand, gaining publicity that money literally could not buy. No promotional video for the UK could conceivably do what this wedding does.

Unlike that other great European resort, Paris, London is not just a place that people visit; they also come to work. It is a resort where people work as well as play. The London commuter region has the largest number of non-national professionals anywhere in the world. Putting on a show like this anchors and reinforces this role.

But the plain fact is that if the region’s economy prospers it will help the whole economy and in any case this wedding is about the British brand, not just the UK one.

Any tally of the additional money spent by visitors, setting that off against the loss of output because of the extra bank holiday, does have a dismal ring to it. But what lifts the whole matter to a different level is the value and role of a brand. On its ability to attract a global television audience, the British Royal family would appear to be the greatest brand on earth. But is it worth anything?

On conventional arithmetic the impact of the wedding on the economy looks to be broadly neutral, maybe slightly positive. On the one hand it is disruptive, not just because of the extra day of holiday but because it comes in the middle of a whole wodge of extra days off, with the late Easter jumbling up with the early May bank holiday. You would normally expect any lost output to be recovered quickly, as common sense would suggest. But if you look back at the precedent of the Queen’s Golden Jubilee in June 2002, there was indeed a sharp fall in industrial output that was not immediately offset by subsequent gains.

On the other hand, the wedding is global in a way the jubilee was not and the commercial sector in London has responded vigorously to the occasion, with all sorts of incentives for visitors to part with their cash. There has been a boom in tourist numbers with estimates varying from 200,000 to 600,000 extra visitors. And I suppose all those foreign news crews who were developing coverage for the two billion viewers must have spent a fair amount extra too.

PricewaterhouseCoopers (PwC) has attempted to put some numbers on this whole thing, estimating that some 550,000 people will witness the event in or around Westminster; that 560,000 people will have travelled to the capital and that the commercial benefit to the London economy would be £107m. That is helpful, particularly at a time such as this, but it is not huge in the context of a regional economy of upwards of £200bn a year. It depends on how you measure it, but I saw calculations recently that ranked the London economy as the third-largest in the world, behind only New York and Tokyo. PwC notes that the Olympics next year is expected to attract more than 10 times the number of visitors, and that they will stay for around a fortnight, not just a day.

Put all this together and I would guess that there is a net plus, particularly to London, but it will not be huge in the context of the whole economy. But in the longer term it reinforces the British brand, gaining publicity that money literally could not buy. No promotional video for the UK could conceivably do what this wedding does.

Unlike that other great European resort, Paris, London is not just a place that people visit; they also come to work. It is a resort where people work as well as play. The London commuter region has the largest number of non-national professionals anywhere in the world. Putting on a show like this anchors and reinforces this role.

But the plain fact is that if the region’s economy prospers it will help the whole economy and in any case this wedding is about the British brand, not just the UK one.

Atlantic International Partnership Headlines:Japan’s Economy Struggles for Air

http://altlanticinternationalpartnership.net/2011/05/loading-symbols-authors-japans-economy-struggles-for-air/

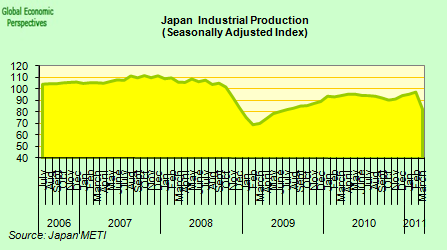

With the arrival of the first real Japanese data since the tsunami struck, the immensity of the tragedy which Japan is passing through is only now gradually becoming apparent. Exports were down by a seasonally adjusted 7.7% in March over February, while imports only fell by a much more modest 1.4%, with the inevitable consequence that the trade surplus, which forms the lifeline for Japan’s fragile economy, shrank sharply. In particular car production was badly hit, with output at Toyota (TM) plunging 62.7% during the month, while Nissan (NSANF.PK) reported a drop of 52.4% and Honda (HMC) put the shrinkage in its Japanese domestic production at 62.9% – adding that output would be at 50 percent of its former projections until at least the end of June.

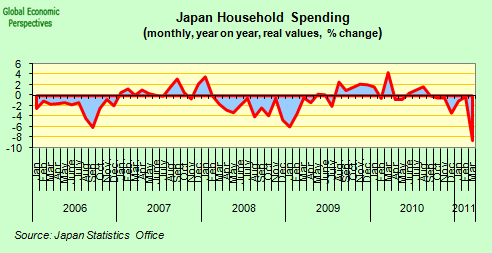

In fact March output across the whole of Japanese industry fell at a record monthly pace of 15.3%, while household spending declined at the record annual rate of 8.5%.

Large as they are, however, these numbers were to some extent expected. More worrisome from the Japanese point of view is the fact that production may be many months getting back to earlier levels given supply chain problems and the fact that electricity generating capacity will remain problematic, leading to reductions in the level of power available.

These delays in restoring production in Japan’s auto industry at a time of substantial economic growth in potential new markets raise the prospect that some of the damage may be permanent, as some part of the Japanese market share goes to the country’s main competitors. Indeed just this point was raised by S&P recently when it cut its outlook to negative for all three manufacturers along with suppliers Aisin Seiki (ASEKF.PK), Denso (DNZOF.PK) and Toyota Industries (TYIDY.PK). In their report justifying the move S&P stated: “The outlook revisions also reflect our opinion that extended production cuts may erode Japanese automakers’ market shares and competitive positions in the longer term.”

Among companies that may well inadvertently benefit from Japan’s ill fortune is the US is General Motors (GM), which less than two years after declaring themselves bankrupt now seems poised to reclaim the global auto sales number one spot from struggling rival Toyota. Japan’s car manufacturers have also been hurt by the sharp rise in the value of the yen. After years of a weak yen boosting sales and corporate profits, the Japanese currency has steadily strengthened to 81 yen to the dollar from 112 at the end of 2007. What might have been seen as a temporary development now looks much more permanent, and strategic planning by Japanese corporates will undoubtedly be influenced by this when it comes to decisions on where to locate new plant and capacity. And in the meanwhile, they stand to loose market share in both the US and in the key growth market, China.

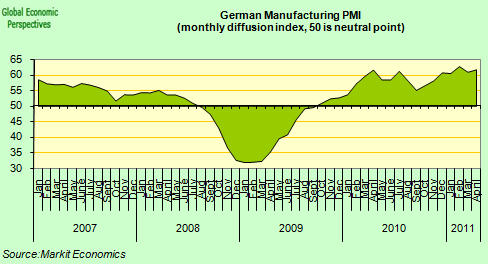

German manufacturing is also an indirect beneficiary of Japan’s ills, and the German April manufacturing PMI once more revealed a very strong performance, underpinned by ex-European demand for capital and intermediate goods.

Obviously the substantial under-performance will continue, as was confirmed by the April manufacturing PMI, which showed a second month of sharp contraction with the indicator registering 45.7 and reflecting a deterioration on the already sharp contraction (46.4) registered in March (50 marks the neutral, or no change mark on these indexes). And while after years of deflation and slow growth Japan’s economy may not be what it used to be, it is still the world’s third largest, so it should not surprise us if JPMorgan attributed a large part of the fall in its March Global Composite PMI (to a six monthly low of 54.7) to the Japan impact. Without the contraction in Japan, it suggests, the Global Output Index reading would have been in the region of 57.3.

On the other hand, since Japan is an export surplus country, and it is highly likely that the slack left by Japan’s export losses will be taken up by its main competitors, beyond a short-lived supply chain blip there is unlikely to be any major impact on Global economic growth in 2011, following from the disaster. The problem here is very much a Japanese one.

We also now have details of the first instalment of money allocated by the government for the reconstruction programme. As expected the initial spending is modest in relation to the extent of the damage, with an emergency budget of 4 trillion yen ($48.5 billion) while total costs have been estimated as lying more in the region of $300 billion. Further, the government has been at pains to stress that no new debt will be issued to cover this spending, and that the resources will be found from cuts in social programmes and from pension fund resources.

In fact the package has been financed using 2.5 trillion yen from the country’s pension funds plus money originally intended to increase payments to families with children. Ironically this money had been promised as part of a campaign to try to address the country’s long term demographic shortfall, which is now playing a key role in generating the country’s evident economic imbalances. In any event, these are hardly “stimulus” measures, although paying for the next round of reconstruction will be much harder without recourse to a new debt issue.

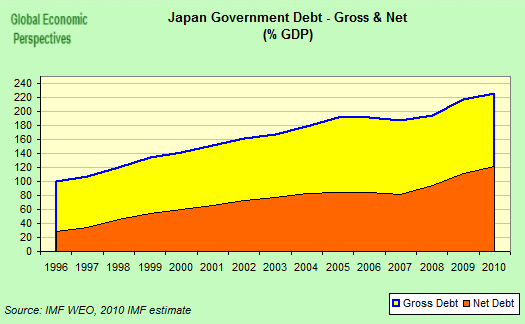

Significantly, no decision seems yet to have been taken on whether to increase consumption tax, since given the ongoing weakness in Japan domestic consumption the application of such a remedy in the current environment may create as many issues as it resolves. The reticence of the Japanese authorities to raise new debt is comprehensible given the fact that the IMF estimates that gross government debt will hit 229% of GDP in 2011 (and net government debt 128%) while the rating agencies are waiting in the wings waving imminent downgrade warnings. Subsequent packages are likely to prove far more challenging in terms of financing, and markets are liable to remain nervous.

It is now more or less universally acknowledged that Japan is in recession, and Bank of Japan governor Masaaki Shirakawa has confirmed this impression by asserting the bank’s view that the economy will continue to contract throughout the first half of the year. In fact only last Saturday he described the country’s economic outlook as “very severe” and asserted that the central bank was resolute in its determination to take appropriate action to support the economy. Most observers interpret this as meaning that the bank will ease further by increasing its asset purchase programme. The BOJ eased policy in the days following the tsunami by doubling to 10 trillion yen the funds it sets aside for purchases of a range of financial assets, such as government bonds and corporate debt, and despite the fact that a proposal from Deputy Governor Kiyohiko Nishimura to expand the programme by 5 trillion yen ($62 billion) was outvoted by the board, the mere fact it was discussed could mean that bank could loosen policy further as early as next month.

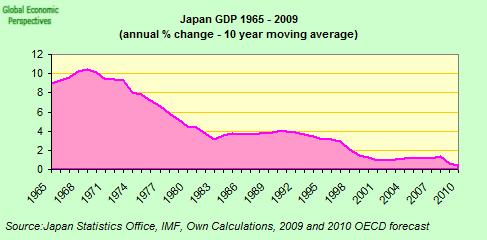

It is important to bear in mind that Japan’s recovery from the global crisis was always fragile, and that while post-Lehman growth resumed in Q2 2009, the economy contracted again in Q3 2009, and suffered a further relapse in Q4 2010. At the end of last year economic activity in Japan was still at the same level as in Q1 2006, and the short term impact of the tsunami will only have served to blow it further back in time.

Thus while it seems pretty clear that growth in Japan will resume in the second half of the year, and that the rebound in the manufacturing industry will be pronounced once a normal power supply is restored, the thesis that natural disaster shocks are invariably good for economies with a lethargic track record of pronounced under-performance seems rather questionable. It is entirely possible that Japan will turn into a reference-case-example of a country where this does not happen (particularly given the major differences in the demographic profile between Post WWII Japan and the country today). In addition, while additional government indebtedness and burden sharing from the private sector may well be short term growth positive, the stimulus will be short lived, since what Japan needs is not a “one off” push start, but major structural changes and in particular a new openness to immigration.

Further down the road only lie major tax increases (which will surely slow the domestic economy even further) or (ultimately) debt restructuring, since surely, even in the Japan case, the sky is not the limit for sovereign debt, and while any Japan sovereign restructuring would have little external impact given that the Japanese are the main holders of their own debt, Japan’s banks (which hold the lion’s share) would hardly escape unscathed. But beyond immediate government debt-woe issues, the big question is the extent to which lasting damage is being done to demand for Japanese home-grown products, and whether or not this will make it more rather than less difficult to sustain in the longer term the external surplus the country so badly needs to underpin its fiscal survival.

With the arrival of the first real Japanese data since the tsunami struck, the immensity of the tragedy which Japan is passing through is only now gradually becoming apparent. Exports were down by a seasonally adjusted 7.7% in March over February, while imports only fell by a much more modest 1.4%, with the inevitable consequence that the trade surplus, which forms the lifeline for Japan’s fragile economy, shrank sharply. In particular car production was badly hit, with output at Toyota (TM) plunging 62.7% during the month, while Nissan (NSANF.PK) reported a drop of 52.4% and Honda (HMC) put the shrinkage in its Japanese domestic production at 62.9% – adding that output would be at 50 percent of its former projections until at least the end of June.

In fact March output across the whole of Japanese industry fell at a record monthly pace of 15.3%, while household spending declined at the record annual rate of 8.5%.

Large as they are, however, these numbers were to some extent expected. More worrisome from the Japanese point of view is the fact that production may be many months getting back to earlier levels given supply chain problems and the fact that electricity generating capacity will remain problematic, leading to reductions in the level of power available.

These delays in restoring production in Japan’s auto industry at a time of substantial economic growth in potential new markets raise the prospect that some of the damage may be permanent, as some part of the Japanese market share goes to the country’s main competitors. Indeed just this point was raised by S&P recently when it cut its outlook to negative for all three manufacturers along with suppliers Aisin Seiki (ASEKF.PK), Denso (DNZOF.PK) and Toyota Industries (TYIDY.PK). In their report justifying the move S&P stated: “The outlook revisions also reflect our opinion that extended production cuts may erode Japanese automakers’ market shares and competitive positions in the longer term.”

Among companies that may well inadvertently benefit from Japan’s ill fortune is the US is General Motors (GM), which less than two years after declaring themselves bankrupt now seems poised to reclaim the global auto sales number one spot from struggling rival Toyota. Japan’s car manufacturers have also been hurt by the sharp rise in the value of the yen. After years of a weak yen boosting sales and corporate profits, the Japanese currency has steadily strengthened to 81 yen to the dollar from 112 at the end of 2007. What might have been seen as a temporary development now looks much more permanent, and strategic planning by Japanese corporates will undoubtedly be influenced by this when it comes to decisions on where to locate new plant and capacity. And in the meanwhile, they stand to loose market share in both the US and in the key growth market, China.

German manufacturing is also an indirect beneficiary of Japan’s ills, and the German April manufacturing PMI once more revealed a very strong performance, underpinned by ex-European demand for capital and intermediate goods.

Obviously the substantial under-performance will continue, as was confirmed by the April manufacturing PMI, which showed a second month of sharp contraction with the indicator registering 45.7 and reflecting a deterioration on the already sharp contraction (46.4) registered in March (50 marks the neutral, or no change mark on these indexes). And while after years of deflation and slow growth Japan’s economy may not be what it used to be, it is still the world’s third largest, so it should not surprise us if JPMorgan attributed a large part of the fall in its March Global Composite PMI (to a six monthly low of 54.7) to the Japan impact. Without the contraction in Japan, it suggests, the Global Output Index reading would have been in the region of 57.3.

On the other hand, since Japan is an export surplus country, and it is highly likely that the slack left by Japan’s export losses will be taken up by its main competitors, beyond a short-lived supply chain blip there is unlikely to be any major impact on Global economic growth in 2011, following from the disaster. The problem here is very much a Japanese one.

We also now have details of the first instalment of money allocated by the government for the reconstruction programme. As expected the initial spending is modest in relation to the extent of the damage, with an emergency budget of 4 trillion yen ($48.5 billion) while total costs have been estimated as lying more in the region of $300 billion. Further, the government has been at pains to stress that no new debt will be issued to cover this spending, and that the resources will be found from cuts in social programmes and from pension fund resources.

In fact the package has been financed using 2.5 trillion yen from the country’s pension funds plus money originally intended to increase payments to families with children. Ironically this money had been promised as part of a campaign to try to address the country’s long term demographic shortfall, which is now playing a key role in generating the country’s evident economic imbalances. In any event, these are hardly “stimulus” measures, although paying for the next round of reconstruction will be much harder without recourse to a new debt issue.

Significantly, no decision seems yet to have been taken on whether to increase consumption tax, since given the ongoing weakness in Japan domestic consumption the application of such a remedy in the current environment may create as many issues as it resolves. The reticence of the Japanese authorities to raise new debt is comprehensible given the fact that the IMF estimates that gross government debt will hit 229% of GDP in 2011 (and net government debt 128%) while the rating agencies are waiting in the wings waving imminent downgrade warnings. Subsequent packages are likely to prove far more challenging in terms of financing, and markets are liable to remain nervous.

It is now more or less universally acknowledged that Japan is in recession, and Bank of Japan governor Masaaki Shirakawa has confirmed this impression by asserting the bank’s view that the economy will continue to contract throughout the first half of the year. In fact only last Saturday he described the country’s economic outlook as “very severe” and asserted that the central bank was resolute in its determination to take appropriate action to support the economy. Most observers interpret this as meaning that the bank will ease further by increasing its asset purchase programme. The BOJ eased policy in the days following the tsunami by doubling to 10 trillion yen the funds it sets aside for purchases of a range of financial assets, such as government bonds and corporate debt, and despite the fact that a proposal from Deputy Governor Kiyohiko Nishimura to expand the programme by 5 trillion yen ($62 billion) was outvoted by the board, the mere fact it was discussed could mean that bank could loosen policy further as early as next month.

It is important to bear in mind that Japan’s recovery from the global crisis was always fragile, and that while post-Lehman growth resumed in Q2 2009, the economy contracted again in Q3 2009, and suffered a further relapse in Q4 2010. At the end of last year economic activity in Japan was still at the same level as in Q1 2006, and the short term impact of the tsunami will only have served to blow it further back in time.

Thus while it seems pretty clear that growth in Japan will resume in the second half of the year, and that the rebound in the manufacturing industry will be pronounced once a normal power supply is restored, the thesis that natural disaster shocks are invariably good for economies with a lethargic track record of pronounced under-performance seems rather questionable. It is entirely possible that Japan will turn into a reference-case-example of a country where this does not happen (particularly given the major differences in the demographic profile between Post WWII Japan and the country today). In addition, while additional government indebtedness and burden sharing from the private sector may well be short term growth positive, the stimulus will be short lived, since what Japan needs is not a “one off” push start, but major structural changes and in particular a new openness to immigration.

Further down the road only lie major tax increases (which will surely slow the domestic economy even further) or (ultimately) debt restructuring, since surely, even in the Japan case, the sky is not the limit for sovereign debt, and while any Japan sovereign restructuring would have little external impact given that the Japanese are the main holders of their own debt, Japan’s banks (which hold the lion’s share) would hardly escape unscathed. But beyond immediate government debt-woe issues, the big question is the extent to which lasting damage is being done to demand for Japanese home-grown products, and whether or not this will make it more rather than less difficult to sustain in the longer term the external surplus the country so badly needs to underpin its fiscal survival.

Atlantic International Partnership Headlines:Bin Laden’s Death Reverberates in Media and Economy

http://altlanticinternationalpartnership.net/2011/05/bin-ladens-death-reverberates-in-media-and-economy/

Social media and other news outlets raced to report the demise of terrorist Osama bin Laden, and the impact was even felt in the stock market and oil prices. As TV newsmen floundered waiting for President Barack Obama to announce bin Laden’s death, Twitter reported record tweet volumes. Hackers are expected to take advantage.

The demise of terrorist Osama bin Laden continued to shake up the world on Monday as details spread of a daring raid by U.S. Navy Seals that took out the Al Qaeda leader. There was an early surge in stock prices, and oil initially fell more than three percent, but skepticism about the future of the Middle East soon caused a correction, Reuters reported.

Traditional vs Social Media

The event was also an extravaganza for conventional media as well as emerging social-media communications. TV networks broke into their regularly scheduled programming around 10:40 p.m. Eastern time Sunday night to announce the news after the White House sent out an advisory that President Barack Obama would address the nation. That didn’t happen for almost an hour, leaving correspondents such as Geraldo Rivera of Fox and Wolf Blitzer of CNN awkwardly grasping for information, frequently shifting between commentators and file footage of bin Laden while waiting for details.

Meanwhile, the social-media infrastructure , which was in its infancy when the Sept. 11, 2001, World Trade Center attacks occurred, faced perhaps the biggest worldwide news event since then, except perhaps the election of Obama in 2008.

, which was in its infancy when the Sept. 11, 2001, World Trade Center attacks occurred, faced perhaps the biggest worldwide news event since then, except perhaps the election of Obama in 2008.

Twitter reported a new record of both average tweets per second and an all-time per-second high during the president’s brief speech and the aftermath. “Last night saw the highest sustained rate of tweets ever” at 3,440, the company reported, with a peak of 5,106 around 11 p.m. EDT, when many TV viewers were tuning into the late news.

“Facebook and Twitter are exploding today with comments, reposting of news stories, and a good bit of humor/commentary,” Professor Davis Houck of the Florida State University School of Communication told us. “When the story broke [Sunday] night on social media, I’m guessing many quickly sought out more traditional media, notably television, especially given that President Obama would soon be addressing the nation. As this week begins, though, social media is again buzzing with the latest … news updates and, again, a good bit of humor.”

Hackers Take Advantage

Data-security experts immediately braced for a wave of malware they expect will be unleashed either by Al Qaeda sympathizers or by hackers taking advantage of the tremendous interest in the topic and the resulting traffic.

“We don’t have any examples yet,” wrote Johannes Ulrich on the SANS Technology Institute’s Internet Storm Center blog. “As with any large news event like this, we expect a flurry of e-mails, and likely black-hat search engine operations trying to take advantage of the event to distribute malware.”

One suspicious example, said Ulrich, of the Bethesda, Md.-based cybersecurity school, is a fake image purporting to show a dead bin Laden with a bloody head wound. (No such image was released.)

“Right now, none of the servers hosting it respond,” Ulrich posted. “Some of the sites return SQL errors, indicating that the sites are receiving too much traffic.”

Chet Wisniewski of the global cybersecurity firm Sophos said he is “seeing lots of scams on Facebook, poisoned Google Image Search links, etc. No jihadist cyberwar yet.”

Social media and other news outlets raced to report the demise of terrorist Osama bin Laden, and the impact was even felt in the stock market and oil prices. As TV newsmen floundered waiting for President Barack Obama to announce bin Laden’s death, Twitter reported record tweet volumes. Hackers are expected to take advantage.

The demise of terrorist Osama bin Laden continued to shake up the world on Monday as details spread of a daring raid by U.S. Navy Seals that took out the Al Qaeda leader. There was an early surge in stock prices, and oil initially fell more than three percent, but skepticism about the future of the Middle East soon caused a correction, Reuters reported.

Traditional vs Social Media

The event was also an extravaganza for conventional media as well as emerging social-media communications. TV networks broke into their regularly scheduled programming around 10:40 p.m. Eastern time Sunday night to announce the news after the White House sent out an advisory that President Barack Obama would address the nation. That didn’t happen for almost an hour, leaving correspondents such as Geraldo Rivera of Fox and Wolf Blitzer of CNN awkwardly grasping for information, frequently shifting between commentators and file footage of bin Laden while waiting for details.

Meanwhile, the social-media infrastructure

Twitter reported a new record of both average tweets per second and an all-time per-second high during the president’s brief speech and the aftermath. “Last night saw the highest sustained rate of tweets ever” at 3,440, the company reported, with a peak of 5,106 around 11 p.m. EDT, when many TV viewers were tuning into the late news.

“Facebook and Twitter are exploding today with comments, reposting of news stories, and a good bit of humor/commentary,” Professor Davis Houck of the Florida State University School of Communication told us. “When the story broke [Sunday] night on social media, I’m guessing many quickly sought out more traditional media, notably television, especially given that President Obama would soon be addressing the nation. As this week begins, though, social media is again buzzing with the latest … news updates and, again, a good bit of humor.”

Hackers Take Advantage

Data-security experts immediately braced for a wave of malware they expect will be unleashed either by Al Qaeda sympathizers or by hackers taking advantage of the tremendous interest in the topic and the resulting traffic.

“We don’t have any examples yet,” wrote Johannes Ulrich on the SANS Technology Institute’s Internet Storm Center blog. “As with any large news event like this, we expect a flurry of e-mails, and likely black-hat search engine operations trying to take advantage of the event to distribute malware.”

One suspicious example, said Ulrich, of the Bethesda, Md.-based cybersecurity school, is a fake image purporting to show a dead bin Laden with a bloody head wound. (No such image was released.)

“Right now, none of the servers hosting

Chet Wisniewski of the global

Atlantic International Partnership Headlines:New financial authority to launch tomorrow

http://altlanticinternationalpartnership.net/2011/05/about-us/

Tomorrow morning Sean Hughes will get down to work as the head of the new Financial Markets Authority, an opportunity he says was too good to refuse.

“Our number one priority is to lift investor confidence in the New Zealand market and grow that market. That means getting people comfortable about coming back and investing in the sharemarket and other markets,” he says.

Around $8.5 billion was lost in recent the finance company meltdown, almost $2000 for every New Zealander.

“It’s been a tragedy what’s happened and we accept that,” Mr Hughes says.

“The last eight, 10 years the existing regulator has sort of sat on the fence, I think I’d characterise that as an ambulance at the bottom of the cliff. And a pretty late arriving one at that,” says John Hawkins of the Shareholders’ Association.

The new authority will have extra powers and an increased budget.

A major task will be prioritising dozens of existing inquiries launched by the Securities Commission.

“I think they need to be proactive, they need to be speedy in their processes, they need to be quite aggressive at chasing the people who break the law,” Mr Hawkins says.

The authority is going to demand greater disclosure of the risks people face when they consider making an investment.

“No investment is free of risk, and provided investors understand what risks they are taking, and they get all the right information to understand what those risks are, then I am hoping, and I believe it will be a safer place to invest,” he says.

Mr Hughes says he is keen to encourage people to shift some of their savings from property and term deposits into other investments like the sharemarket – something he says will ultimately help grow the economy and create jobs.

Tomorrow morning Sean Hughes will get down to work as the head of the new Financial Markets Authority, an opportunity he says was too good to refuse.

“Our number one priority is to lift investor confidence in the New Zealand market and grow that market. That means getting people comfortable about coming back and investing in the sharemarket and other markets,” he says.

Around $8.5 billion was lost in recent the finance company meltdown, almost $2000 for every New Zealander.

“It’s been a tragedy what’s happened and we accept that,” Mr Hughes says.

“The last eight, 10 years the existing regulator has sort of sat on the fence, I think I’d characterise that as an ambulance at the bottom of the cliff. And a pretty late arriving one at that,” says John Hawkins of the Shareholders’ Association.

The new authority will have extra powers and an increased budget.

A major task will be prioritising dozens of existing inquiries launched by the Securities Commission.

“I think they need to be proactive, they need to be speedy in their processes, they need to be quite aggressive at chasing the people who break the law,” Mr Hawkins says.

The authority is going to demand greater disclosure of the risks people face when they consider making an investment.

“No investment is free of risk, and provided investors understand what risks they are taking, and they get all the right information to understand what those risks are, then I am hoping, and I believe it will be a safer place to invest,” he says.

Mr Hughes says he is keen to encourage people to shift some of their savings from property and term deposits into other investments like the sharemarket – something he says will ultimately help grow the economy and create jobs.

Subscribe to:

Posts (Atom)